What Is a Public Adjuster? (And When You Actually Need One)

Most homeowners filing a claim assume the insurance company's adjuster is there to help them. They're not. Their job is to figure out what the insurance company owes — which often means finding reasons to pay less. A licensed public adjuster is the only insurance professional who works for the policyholder.

If you've ever wondered who's actually on your side during an insurance claim, this guide explains it in plain English: what a public adjuster does, when hiring one is worth it, what we're allowed to charge in Florida, Minnesota, and Wisconsin, and how to verify any PA before you sign anything.

Free 15-minute claim review

Not sure if a public adjuster can help with your claim? We'll tell you straight — including when we don't think you need us.

Talk to a licensed PA →The three types of insurance adjusters (and whose side they're on)

Every property insurance claim involves at least one adjuster. Understanding which type you're dealing with — and who pays them — is the foundation of everything that follows.

1. The insurance company adjuster (staff adjuster)

This is the adjuster your insurance company assigns to your claim when you file it. They're a salaried employee of the insurer. Their job is to evaluate the loss, determine what the policy covers, and recommend a settlement amount.

Staff adjusters aren't dishonest people. But the financial incentive is structural: their employer profits when claims close for less. Their performance reviews, bonuses, and promotions are tied to keeping claim costs down.

2. The independent adjuster

When an insurance company has too many claims for staff adjusters to handle (after a hurricane, for example), they hire independent adjusters on contract. Independent adjusters work freelance — but they're hired and paid by the insurance company. They report to the insurer, not the policyholder.

Most homeowners don't realize the "independent adjuster" who shows up after a major weather event isn't independent in the way the name suggests. They're independent contractors of the insurer.

3. The public adjuster

A public adjuster is the only adjuster type licensed by the state to represent the policyholder. We assess the damage independently, document the loss, build the claim file, and negotiate the settlement on your behalf.

Public adjusters are paid on contingency — a percentage of what we recover. The financial incentive runs in your direction: a bigger settlement means a bigger fee, which means we're aligned with you, not the insurance company.

The structural difference: Insurance company adjusters and independent adjusters both work for the insurance company. Public adjusters are the only ones licensed to work for the homeowner. That's not opinion — that's how state insurance law defines the roles.

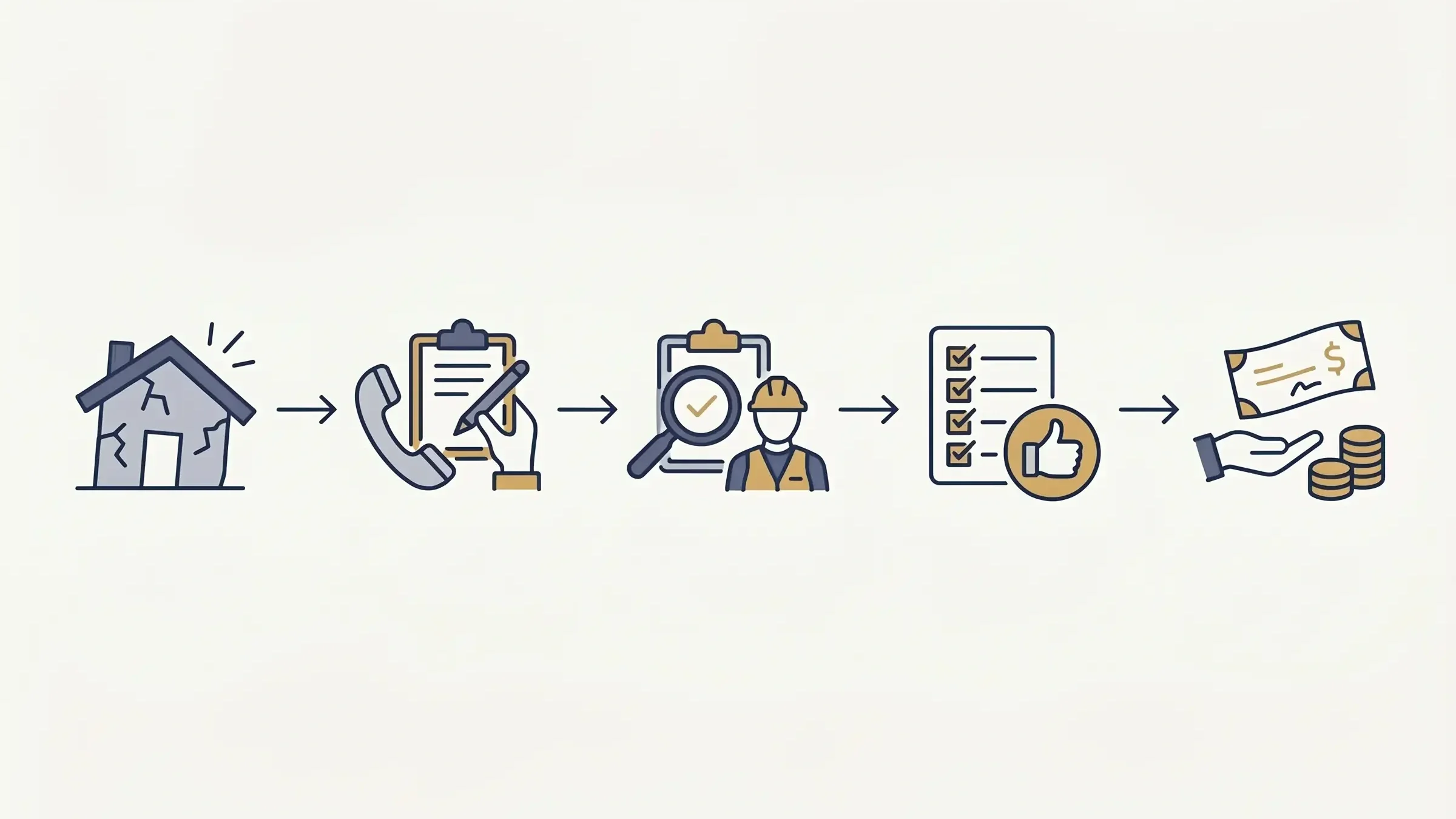

What public adjusters actually do, step by step

"Public adjuster" is one of those professional titles that doesn't tell you much about the actual work. Here's what we do on a typical residential claim, in order:

- Free initial review. You send us your denial letter, settlement offer, or just the facts of your loss. We tell you whether we think we can help — and whether the math makes sense for you to hire a PA.

- Policy and claim file analysis. We read your full policy (most homeowners haven't), the insurer's claim file, and any inspection reports. This usually surfaces coverages the insurer hasn't applied or exclusions that don't actually apply to your loss.

- Independent damage assessment. We inspect the property ourselves — sometimes with engineers, industrial hygienists, or contractors. Our scope of loss often differs significantly from the insurer's.

- Documentation and proof of loss. We assemble photos, contractor estimates, expert reports, and the formal proof-of-loss document the insurer requires. Most underpayments happen because the homeowner couldn't document the full scope.

- Claim negotiation. We negotiate directly with the insurance company adjuster. This is where most of the recovery happens — they have a number, we have a number, and we work toward a settlement.

- Escalation if needed. If negotiation stalls, we can invoke the appraisal clause (a binding process most policies include), file a state DOI complaint, or refer the case to an attorney for bad-faith litigation.

- Settlement and payout. The insurer issues the check. Our fee comes out of the settlement — you never pay out of pocket.

The whole process typically takes 30 to 90 days for straightforward claims, longer for complex losses or disputed denials.

When hiring a public adjuster makes sense (and when it doesn't)

Counter-intuitive truth: not every claim needs a public adjuster. We tell people that on first calls. Here's the honest breakdown.

When a PA usually pays for itself

- The claim is denied. A denial isn't usually final. Most denials get overturned with proper documentation and the right appeal process. PAs do this work daily.

- The settlement offer feels low. If the insurer's first offer doesn't match what your contractor says it will cost to fix the property, the gap is usually negotiable.

- The loss is over $25,000. Larger claims have more components, more places for the insurer to underpay, and more leverage for a PA to find recovery. The contingency fee math works clearly in your favor.

- The damage is complex. Multiple perils (wind plus flood, water plus mold), structural damage, code-required upgrades, or claims involving high-value contents — all benefit from PA expertise.

- The insurer is dragging the claim. Florida law (F.S. 627.70131) requires insurers to acknowledge claims within 14 days and pay or deny within 60 days of receiving your proof of loss — or 90 days for hurricane and Governor-declared emergency claims. If they're missing those deadlines, a PA's involvement often accelerates the timeline.

When a PA probably isn't worth it

- The claim is small. Under $5,000 in damage, the contingency fee may not produce enough net benefit to justify hiring a PA.

- The insurer is paying full freight on the first offer. If the offer matches your contractor estimates and there's no dispute, you don't need representation.

- You've already cashed the settlement check. Once you've signed a release, the claim is typically closed. There are exceptions (supplemental claims), but the leverage is mostly gone.

The OPPAGA evidence: Florida's Office of Program Policy Analysis (Report 10-06, January 2010) found that PA-represented policyholders received settlements 747% higher on 2005 hurricane claims and 574% higher on non-catastrophe claims (median $9,379 with a PA vs $1,391 without) than unrepresented claims. Two honest caveats from the report itself: (1) those are gross settlement differences, before the PA's contingency fee — your net pocket gain is lower; (2) selection bias matters — PAs are typically hired on harder claims (denied, partial, complex), which get more scrutiny regardless. PAs don't inflate every claim. They produce recovery on claims where recovery was being missed.

How public adjusters get paid (and what's legal in each state)

Every state regulates public adjuster fees differently. Here's what's enforceable in our three service states:

| State | Standard fee cap | Catastrophe rate | Statute |

|---|---|---|---|

| Florida | 20% of claim payout (non-emergency) | 10% during the year after a Governor-declared emergency | F.S. 626.854(11)(b) |

| Minnesota | No statutory cap (typical market rate: 10–15%) | n/a | MN insurance code |

| Wisconsin | Negotiable for non-catastrophe claims | 10% during officially declared catastrophes | WI Stat. 628.34 |

Three things to know that aren't on the table:

- No upfront fees. Anywhere. A PA who asks for retainer or hourly is not following industry norms — walk away.

- If we don't recover, you don't pay. Pure contingency. The fee comes out of the settlement check, not your pocket.

- Florida flat fees exist for a specific case. Following the 2024 Parrish ruling, contingency-fee PAs cannot serve as "disinterested" appraisers in Florida auto appraisal-clause work. We use flat-fee arrangements for that specific scope.

The math is straightforward: on a $50,000 settlement, a 20% non-emergency Florida fee is $10,000. After a Governor-declared emergency (most hurricane claims), the cap drops to 10% — so the same settlement carries a $5,000 fee. Minnesota's market typically lands at 10–15%; Wisconsin's catastrophe cap is 10%. Always get the percentage in writing before signing.

Public adjuster vs. attorney vs. doing it yourself

Three common questions we get on first calls:

"Should I just file the claim myself?"

For straightforward small claims, yes — that's often the right answer. The insurance claims process is designed to be navigable by homeowners. Mitigate the damage, document everything, file promptly, follow up if the offer is too low.

The problem isn't whether you can file your own claim. It's whether you'll get paid in full. Insurers count on policyholders accepting first offers. If you're not equipped to push back with documentation and policy analysis, the gap between what you collect and what your claim is worth can be substantial.

"Should I hire a lawyer instead?"

Lawyers are the right call when you need to sue. Bad-faith insurance lawsuits are real causes of action in every state, and good insurance attorneys win them. But litigation is slow (12–24 months), and most claim disputes resolve faster through PA negotiation (30–90 days) before lawsuit becomes necessary.

The smart sequence is usually: PA first, DOI complaint as parallel pressure, then attorney for bad-faith litigation if both fail. We refer cases to attorneys when the insurer's behavior crosses into bad faith and we coordinate with their counsel.

"Can I do both?"

Yes — and it often makes sense on large or complex claims. PAs handle the claim documentation and negotiation; attorneys pursue bad-faith damages when negotiation fails. The PA's documentation becomes the foundation of any subsequent litigation.

How to verify a public adjuster is licensed

Public adjuster fraud exists. So do unlicensed "PAs" working in disaster zones who collect fees and disappear. Always verify the license before signing anything.

Florida

Search at the Florida Department of Financial Services license lookup. Confirm: active license, license type "All-Lines Adjuster" or "Public Adjuster," and no disciplinary actions on record.

Minnesota

Use the Minnesota Department of Commerce licensee lookup. Public adjusters in Minnesota must be individually licensed.

Wisconsin

Use the Wisconsin OCI license lookup. Verify the public adjuster is in good standing.

Our credentials: Shoreline Public Adjusters, LLC holds firm public adjuster licenses in Florida (#G199012), Minnesota (#40962416), and Wisconsin (#21156868). Mitch Miles, our licensed public adjuster, holds individual licenses in Florida (#G117229), Minnesota (#40960638), and Wisconsin (#21156868). Verify any of these directly through the state lookup links above before working with us.

Red flags to walk away from

- Asks for any upfront fee, retainer, or hourly payment

- Won't show you the contract before pressuring you to sign

- Promises a specific dollar recovery before reviewing your claim

- Solicits door-to-door immediately after a disaster (often illegal)

- License number can't be verified through the state lookup

- Won't put fee percentage in writing

What to do next

If you have an active claim — denied, underpaid, or just not feeling right — get a free review before you accept any offer or sign any release. Reviews are no-obligation. If your claim is straightforward and the insurer is paying full freight, we'll tell you.

If you don't have an active claim but want to understand your policy before you need to file one, that's also a free conversation. Most homeowners haven't read their policies and don't know what's covered until something goes wrong. We can walk through it with you.

Get a free claim review

Call (954) 546-1899 or use the form. We'll tell you in 15 minutes whether a public adjuster can help — including when the answer is no.

Start your free review →Frequently asked questions

Is a public adjuster the same as an insurance adjuster?

No. An insurance company adjuster works for the insurer and is paid to limit payouts. A public adjuster is licensed by the state and works for the policyholder on a contingency fee, with the financial incentive to maximize the settlement.

How much does a public adjuster cost in Florida?

Florida Statute 626.854(11)(b) caps public adjuster fees at 20% of the claim payout for non-emergency claims and 10% for claims arising from a Governor-declared state of emergency (during the one-year window after the declaration). There are no upfront fees — PAs are paid as a percentage of what they recover.

Can a public adjuster help with auto insurance claims?

In Florida, yes — licensed public adjusters can assist with diminished value and total loss appraisal-clause work for auto claims. Following the 2024 Parrish ruling, contingency-fee PAs can't serve as "disinterested" appraisers, so flat-fee arrangements are typically used. In Minnesota and Wisconsin, public adjusters generally handle property claims only.

When is it too late to hire a public adjuster?

In most cases, before you've cashed the final settlement check. Once you sign a release and accept payment, the claim is typically closed. If you're unsure, contact a PA for a free review before accepting any insurer offer.

Will hiring a public adjuster slow down my claim?

Typically the opposite. PAs handle documentation, scope of loss preparation, and insurer negotiations — work that homeowners often delay because it's time-consuming. Most PA-handled claims close faster than DIY claims because the process is professionally managed.

Related reading

Shoreline Public Adjusters, LLCEmail: hello@teamshoreline.com

Phone: 954-546-1899

Fax: 239-778-9889