How Much Does a Public Adjuster Cost? (FL, MN & WI Fee Breakdown)

Public adjuster fees are one of the most-asked questions on first calls — and one of the most poorly explained on the internet. Short answer: contingency-only, no upfront cost, capped by statute in Florida and Wisconsin, market-rate in Minnesota. The longer answer, with statute citations and worked math, is below.

This guide explains exactly what a public adjuster can charge in Florida, Minnesota, and Wisconsin — what's enforceable by law, what's negotiable, what to demand in writing before signing, and what red flags mean you should walk away.

Free 15-minute claim review

Want a straight answer on what a PA would cost your specific claim? We'll quote it on the first call — no pressure to hire.

Get a free quote →The short answer: contingency fees, no upfront cost

Every legitimate public adjuster in the United States works on a contingency fee basis. That means three things:

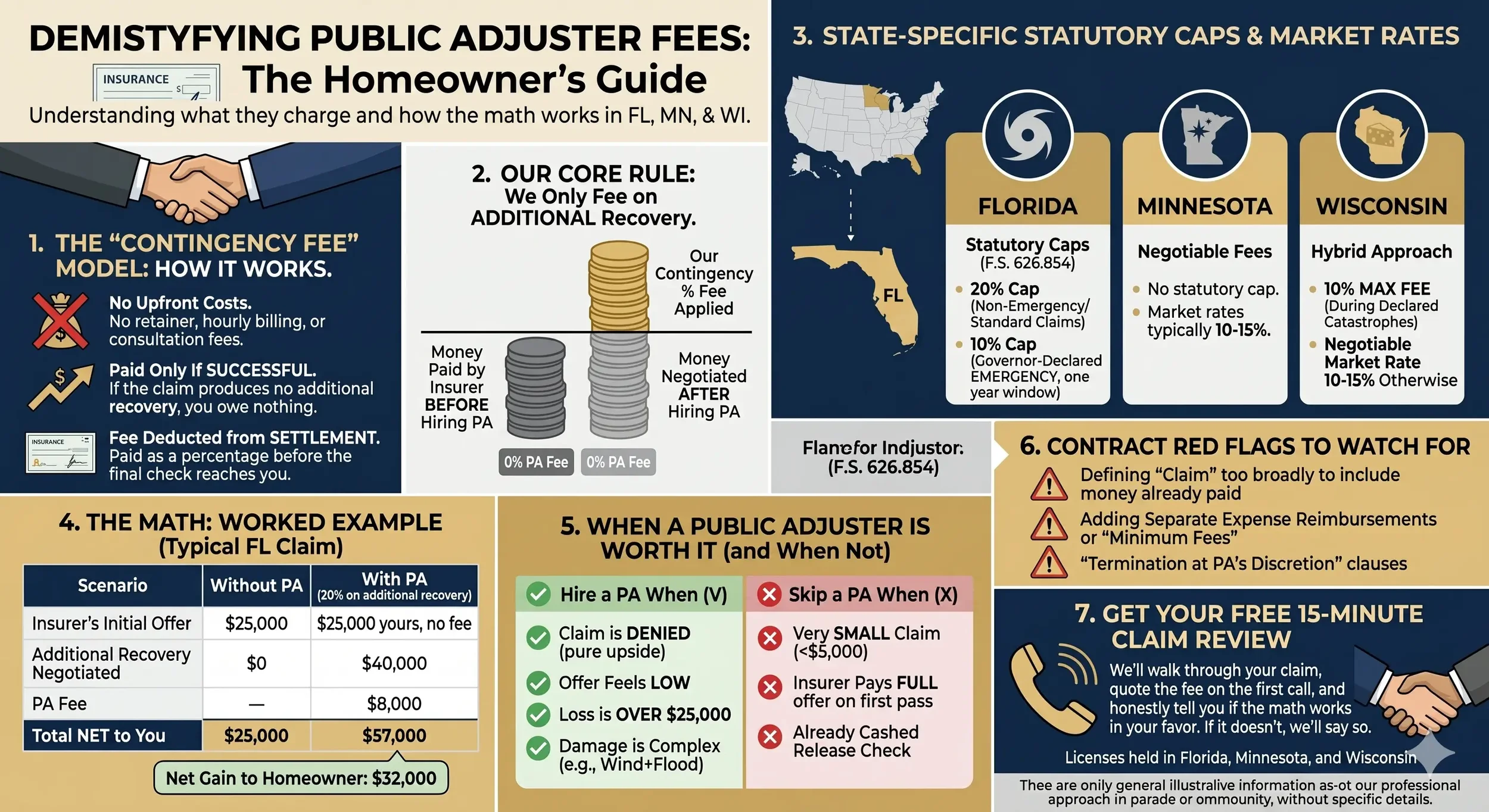

- No upfront payment. No retainer, no hourly billing, no consultation fee.

- You pay only if we recover. If the claim doesn't produce additional money, you owe nothing.

- The fee comes out of the settlement check, not your pocket. When the insurer pays, the PA's percentage is deducted before the remainder reaches you.

The percentage is the variable, and it depends on which state you're in, whether the loss came from a declared emergency, and what the contract specifies. Florida sets the strictest statutory caps. Wisconsin caps fees only during catastrophes. Minnesota leaves the percentage open to negotiation.

One nuance worth knowing: our fee applies only to amounts we recover after you hire us. Any payments your insurance carrier made before the agreement is signed are yours — we take no fee on those funds. The PA earns only on the additional money secured beyond what the insurer had already paid.

Florida public adjuster fees (F.S. 626.854 explained)

Florida regulates public adjuster fees more strictly than any other state. The relevant statute is F.S. 626.854(11)(b), and it sets two distinct caps:

- 20% of the claim payout for non-emergency claims (the standard rate)

- 10% of the claim payout for claims arising from a Governor-declared state of emergency, during the one-year window after the declaration

The 10% emergency rate is policyholder protection. After major hurricanes, public adjusters and unlicensed solicitors flood disaster zones — the lower cap reduces price-gouging on homeowners in crisis. The standard 20% rate applies to all other claims (water damage, fire, mold, hail outside a declared emergency, etc.).

The fee is calculated on the amount the insurer pays as a result of the claim, not the total damage estimate. If we recover $50,000 on a non-emergency claim, our fee is $10,000 (20%). If we recover $50,000 on a hurricane claim within the emergency window, our fee is $5,000 (10%).

Important Florida exception: following the 2024 Parrish ruling, contingency-fee public adjusters cannot serve as "disinterested" appraisers in Florida auto appraisal-clause work. For auto claims involving the appraisal clause, we use flat-fee arrangements instead of contingency. For all property claims (residential, commercial, HOA), contingency remains the standard.

Minnesota public adjuster fees

Minnesota does not cap public adjuster fees by statute. The percentage is negotiable between the policyholder and the PA — and that negotiation should happen in writing, before you sign the contract.

Market-rate Minnesota contracts typically land in the 10–15% range for property claims. Larger losses sometimes negotiate down (10–12%); complex multi-peril claims sometimes settle higher (12–15%). The absence of a statutory cap doesn't mean PAs can charge anything they want — the open market keeps rates reasonable, and excessive fees can be challenged as unconscionable under Minnesota contract law.

Minnesota requires public adjusters to be individually licensed through the Department of Commerce. Always verify the license before signing — see the MN licensee lookup.

Wisconsin public adjuster fees (catastrophe vs non-catastrophe)

Wisconsin takes a hybrid approach: fees are capped only during officially declared catastrophes, and negotiable otherwise.

- During declared catastrophes: 10% maximum fee (similar to Florida's emergency cap, for the same protective reason)

- All other claims: negotiable, with market rates typically 10–15%

Wisconsin's "catastrophe" designation is made by the state government and applies for the duration of the declared event. Outside of those windows, the fee is contractually open. Verify any Wisconsin public adjuster's license at the Wisconsin OCI license lookup before signing.

What "contingency fee" actually means in practice

The contingency model aligns the public adjuster's incentive with yours: bigger settlement means bigger fee, which means the PA is motivated to maximize the recovery. But the structure has practical mechanics that catch some homeowners off guard. Here's how it actually works:

How the fee gets paid

When the insurance company issues the settlement check, one of two things happens depending on the carrier:

- Single check to a trust account. The insurer issues one check made out to the PA's trust account. The PA deducts the agreed percentage and disburses the remainder to the policyholder. Most common setup.

- Two separate checks. Some insurers issue separate payments — one directly to the policyholder for their portion, one to the PA for the fee. Less common but increasingly used post-2022.

Either way, you never write a check to the PA out of your own funds. The fee comes from the recovered settlement only.

What the fee is calculated on

The fee applies to amounts the PA recovers after you sign the agreement. This is the part most homeowners miss:

- If the insurer paid you $20,000 before you hired a PA, that $20,000 is yours. The PA takes no fee on it.

- If the PA then negotiates an additional $40,000 supplemental payment, the fee applies to the $40,000 — not to the original $20,000 plus $40,000.

- So a 20% Florida fee on the supplemental recovery would be $8,000, leaving the policyholder with $52,000 of the additional $60,000 total settlement.

This honest distinction matters: a PA who claims to charge "20% of the total claim" is overreaching if the insurer had already issued payment before the PA was hired. Always read the contract for the language that defines what the fee applies to.

Worked math: a typical Florida non-emergency claim

| Scenario | Without PA | With PA (20% on additional recovery) |

|---|---|---|

| Insurer's initial offer | $25,000 | $25,000 (yours, no fee) |

| Additional recovery negotiated | $0 | $40,000 |

| PA fee (20% of additional) | — | $8,000 |

| Total to you | $25,000 | $57,000 |

In this scenario, the homeowner's net pocket gain from hiring the PA is $32,000 ($57K − $25K). That's the math that decides whether contingency makes sense for your specific claim.

When the PA fee is worth it (and when it isn't)

Contingency fees aren't free money — they're a fixed cost on additional recovery. The honest question is whether the additional recovery exceeds the fee enough to make hiring worthwhile. Here's the breakdown:

When the math typically works in your favor

- The claim is denied. $0 → any recovery is pure upside. Contingency fee math always works on denied claims.

- The settlement offer feels low. Independent damage assessment usually finds 30-100%+ underpayment. Even with the fee, your net pocket gain is substantial.

- Loss is over $25,000. Larger claims have more places for the insurer to underpay (code upgrades, ALE, contents replacement cost vs ACV, depreciation disputes). The dollar absolute of additional recovery typically exceeds the fee multiple times over.

- Multi-peril or complex damage. Wind plus flood, water plus mold, fire plus smoke — every additional peril is an additional negotiation. PAs find recovery in the gaps.

When the math probably doesn't work

- Very small claims (under $5,000). Even if the PA finds 50% additional recovery, the fee may eat most of the gain. Often easier to file yourself.

- Insurer is paying full freight on the first offer. If the offer matches your contractor estimates and there's no dispute, there's nothing for the PA to recover.

- Already cashed the settlement check. Once you've signed a release, the claim is typically closed. Limited room for supplemental claims in most cases.

The OPPAGA evidence on PA value: Florida's Office of Program Policy Analysis (Report 10-06, January 2010) found that PA-represented policyholders received settlements 747% higher on 2005 hurricane (Wilma) claims and 574% higher on non-catastrophe claims (median $9,379 with a PA vs $1,391 without). The report's own caveat: those are gross settlement differences before the PA's fee — net pocket gain is lower. But even after a 20% fee, the OPPAGA non-catastrophe math leaves the policyholder with ~$7,500 vs $1,391 without representation. The fee earns out on most non-trivial claims.

Hidden costs to watch for (other PAs, not us)

Most PA fee transparency issues come from contract language, not the headline percentage. Things to look for in any PA contract before signing:

- What does "claim" actually mean in the contract? Some PAs define it broadly enough to claim a fee on the entire settlement (including pre-existing payments). The honest version: fee applies only to additional recovery after signing.

- Are there expense reimbursements separate from the fee? Some contracts add line items for engineer reports, expert testimony, photo documentation. These should be disclosed upfront. Our practice: expenses are bundled into the contingency fee unless explicitly negotiated.

- What happens if the claim is denied entirely? Should be: you owe nothing. Some contracts try to charge a "minimum fee" or "documentation fee" even on denied claims. Walk away from those.

- Can the PA quit the case midway? Reputable PAs commit to seeing the claim through. Watch for "termination at PA's discretion" clauses that let them walk away after collecting easy money.

- What's the cancellation window? Most states require a cancellation period (Florida is 3 business days) during which you can cancel without penalty. Make sure your contract honors it.

How to verify our fees before signing

Three things to do before signing any public adjuster contract — including ours:

- Verify the license at the state DOI lookup (FL, MN, WI). Confirm the license is active and the firm name matches what's on the contract.

- Read the fee paragraph carefully. Confirm the percentage matches what was discussed. Confirm the fee applies only to additional recovery after signing. Confirm there are no separate expense reimbursements.

- Get a written quote on a sample claim. Ask the PA to walk you through the math on a hypothetical claim similar to yours. If they can't or won't, that's a red flag.

Our credentials: Shoreline Public Adjusters, LLC holds firm public adjuster licenses in Florida (#G199012), Minnesota (#40962416), and Wisconsin (#21156868). Mitch Miles, our licensed public adjuster, holds individual licenses in Florida (#G117229), Minnesota (#40960638), and Wisconsin (#21156868). Verify any of these directly through the state lookup links above before working with us.

What to do next

If you have an active claim and want a straight answer on what hiring a PA would cost — not a sales pitch, just the math — get a free 15-minute review. We'll walk through your specific claim, quote the fee, and tell you honestly whether the math works in your favor. If it doesn't, we'll say so.

Get a free fee quote on your claim

Call (954) 546-1899 or use the form. We'll quote the fee on the first call and tell you straight whether it's worth hiring.

Get your free quote →Frequently asked questions

How much does a public adjuster charge in Florida?

Florida Statute 626.854(11)(b) caps public adjuster fees at 20% of the claim payout for non-emergency claims, and 10% for claims arising from a Governor-declared state of emergency (during the one-year window after the declaration). There are no upfront fees, hourly charges, or retainers — Florida public adjusters are paid only as a percentage of what they recover for you.

Do public adjusters charge upfront fees?

No. Anywhere in the country, a legitimate public adjuster works on contingency — paid only as a percentage of what they recover. Any PA who asks for an upfront fee, retainer, or hourly payment is operating outside industry norms. Walk away.

What if a Florida public adjuster wants to charge a flat fee instead of a percentage?

Flat fees are legal in Florida and are most commonly used for auto appraisal-clause work. Following the 2024 Parrish ruling, contingency-fee public adjusters cannot serve as "disinterested" appraisers in Florida auto claims, so flat-fee arrangements are now standard for that specific scope. For property claims, contingency is the norm.

Are public adjuster fees taken from your payout or paid separately?

The fee is taken directly from the settlement check — you never pay out of pocket. When the insurer issues payment, it typically goes through a trust account where the PA's percentage is deducted before the remainder reaches you. Some insurers issue separate checks (one to the policyholder, one to the PA). Either way, the fee never comes from your existing assets.

Will you charge me on money the insurance company already paid before I hired you?

No. Our fee applies only to amounts we recover after you hire us. Any payments your insurance carrier made before our agreement is signed are yours, and we take no fee on those funds. We only get paid when we secure additional money beyond what was already paid.

What's the maximum a Wisconsin public adjuster can charge?

Wisconsin caps public adjuster fees at 10% of the claim payout only during catastrophes officially declared by the Governor. Outside of declared catastrophes, fees are negotiable between the policyholder and the public adjuster. Most market-rate Wisconsin contracts land at 10-15% for non-catastrophe work.

Related reading

Shoreline Public Adjusters, LLCEmail: hello@teamshoreline.com

Phone: 954-546-1899

Fax: 239-778-9889